ICARA Statement

Vs 2021-2022

ICARA weatherXchange Limited ("WXL/ the Firm")

Summary

WXL is authorised and regulated by the Financial Conduct Authority and approved as an Introducing Broker (IB) by the CFTC in the US.

WXL is a Small Non-Interconnected ("SNI") MIFIDPRU investment firm, as explained in Chapter I of the Firm’s Compliance Procedures Manual. As such, under MIFIDPRU 7, it is required to undertake a review of its Internal Capital Adequacy and Risk Assessment ("ICARA") Process at least annually (MIFIDPRU 7.8.2R) and to document the review (MIFIDPRU 7.8.7R).

Full details of the Firm’s obligations under MIFIDPRU 7 are to be found in the Firm’s Statement of the ICARA Process and Document.

The ICARA Document is required to contain at least the following information:-

- a summary of material harms identified by the firm and any steps taken to mitigate them;

- a clear explanation of how the firm is complying with the OFAR, including a clear breakdown of the following as at the review date:

- available own funds;

- available liquid assets;

- the firm’s assessment of its threshold requirements; and

- the levels of own funds and liquid assets that, if reached, the firm has identified may indicate that there is a credible risk that the firm will breach its threshold requirements.

As a former BIPRU/Exempt CAD firm, the Firm is taking advantage of the transition arrangements whereby its Permanent Minimum Requirement ("PMR") will be £50k in 2022 rising by £5k each year until it reaches £75k. It is also taking advantage of the ability for its fixed overhead requirement "(FOR") to be capped at twice the PMR for the first five years.

The Firm does not have a regulated UK or foreign holding company as it is not part of a group, and therefore it is not subject to the Prudential Consolidation requirements under MIFIDPRU 2.5 or the Group Capital Test under MIFIDPRU 2.6 (as explained in the Firm’s Compliance Procedures Manual).

The Firm does not have any appointed representative firm.

This Document identifies potential material harms that can be caused by the Firm or can done to the Firm’s business and demonstrates how these harms are mitigated.

Details of potential risk scenarios are set out below.

Key background to this document are the following points:

- WXL takes no positions in any securities.

- WXL handles no client monies

- WXL only occasionally undertakes regulated activities depending on client demand. There have been no direct revenues from regulated activities in the last 10 financial years.

Given the operations of the Firm there is not sensible stress testing to be undertaken. Capital reserves are held by the Firm in cash. However, if the platform for example was to stop operations there would be no financial impact on any customer other than an inability to use the system to send RFPs to potential protections sellers. The platform does not generate direct revenue and its costs are effectively supported by the non-regulated Group.

It is arguable that a customer might argue that they entered into a hedging transaction outside the platform because of incorrect data provided through the platform and therefor look for compensation from the Firm. However, the contractual provisions of use seek to exclude liability for this.

Accordingly, The findings and conclusions of the Firm’s ICARA process are that the Firm is subject to the capped FOR requirements and is complying with the Overall Financial Adequacy Rule ("OFAR").

Details of the wind down plan are set out below. However as noted wind down would not involve potential payment of liabilities to customers given the nature of the Firms operations.

WXL is involved in the following areas of business:

- Provision of a web-based platform to guide end users/hedgers through the process of specifying the terms and conditions of a potential hedge in the form of a Request for Price (RFP). The RFP can be sent to a number of Protection Sellers that are registered on the platform.

- Provision of consultancy and origination services in relation to the placement of weather risk (regulated activity)

WXL is part of the Speedwell group of companies that are involved in the following areas of business:

- Provision of climate data and forecasts (unregulated).

- Provision of software systems in relation to understanding climate risk return periods and managing a portfolio of climate risk-transfer contracts(unregulated)

- Weather station installation (unregulated)

- Provision of settlement data for climate risk-transfer transactions including weather-related and renewables-related benchmarks (unregulated and regulated)

Background

WXL was founded in 1999 as a fully-owned subsidiary of Speedwell Associates Limited (SAL).

Speedwell Climate Corp (SCC) was established in 2007 and is a Delaware-registered corporation trading from Charleston, South Carolina, USA.

In 2012, all non-regulated activities and assets were moved from WXL to Speedwell Climate Ltd (SCL). SCL has an identical ownership structure to WXL. SCC was transferred to SCL as a result of this transferral.

WeatherRiskExchange is a subsidiary of, and wholly owned by, WXL. It is currently dormant.

Together with Speedwell Settlement Services Ltd, these companies form the Speedwell group of companies.

Business Model and Risk Appetite

Details of the business model are set out above. As noted, it is an operational platform and does not involve exposure for customers. Accordingly, there is essentially no material risk exposure for Customers (other than the that related to the quality of data provided)..

Material Harms Identified

No material harms are identified for the Customer. Inability to access the system would not present a material harm for a Customer who could access benefits of weatherXchange use through other more conventional methods.

It is arguable that a Customer might look to argue that they had entered into a hedging transaction on the basis of incorrect data supplied through the weatherXchange platform. However, no transactions are executed on the Platform, the Group has been providing such data for over 20 years and there have been no successful litigations made against any member regulated or not or the Group. The contractual conditions for use of the Platform would seek to limit any such claim.

Capital Position

WXL has no requirement for any external funding and carries no debt. Furthermore, it does not have, nor currently require, an overdraft facility. Short term funding needs are satisfied by carrying a material cash balance. WXL and its parent company have always been operated on an ultra-conservative basis with relatively high cash balances. These have been maintained since the founding of the company.

This philosophy renders us independent of the whim of external capital providers and, therefore, the conditions of the capital markets.

Capital Adequacy

WXL believes that the basic regulatory requirement, although exceeded, is greater than that necessary for prudential running of its business. This is because of the following factors:

- Our regulated activities contribute at most circa 20% to group revenues. In many years this value is much less (inc all years from 2009).

- Within our regulated activities we assume no market risk.

- Within our regulated activities our consultancy and origination function (although not deployed for a decade) operates in a negotiated, order-driven market in which transactions are worked on over a period of weeks rather than seconds. This considerably reduces exposure - we are not exposed to "out trades" that can arise in other voice-brokered liquidity driven markets and which may, in those markets, result from misunderstandings or errors.

- The Speedwell group has a diverse client base (approx 75 clients) in energy, banking, insurance, agriculture and investment funds from the non-regulated part of our activity. Low concentration means we are less exposed to a problem in one sector.

- Speedwell group clients are geographically diversified covering USA, Europe, and Australia making us less exposed to regional problems.

- The majority of our revenue is repeatable based on annual contracts from the non-regulated part of our activity covering, for example, software and weather data or forecast feeds.

The following risk types are now addressed:

Credit Risk

WXL is exposed only to the value of unpaid invoices for its service.

WXL does not act as a principal in its regulated intermediary function.

There have been no bad debts in the last 10 financial years.

Market Risk

None. The weatherXchange Platform is not an execution venue.

Operational Risk

Our activities relate largely to messaging or advisory matters in markets which are not electronically executed. They therefore do not implicate the use of any mission critical systems and do not require us to work from one particular location. Therefore our operational risk in relation to our regulated activity is limited.

Liquidity Risk

WXL takes no positions in securities and has no investments of an illiquid nature. WXL’s cash balance sheet is invested in instant access accounts with banks with UK banking licences.

Insurance Risk

Our insurance covers legal requirements but not professional liability.

Wholesale and Unsecured funding risk:

N/A. We use no external funding

Concentration Risk

The Speedwell group has a relatively large client base in energy, banking, insurance, and investment funds. Low concentration means we are less exposed to a problems in one sector. Our clients are geographically diversified covering USA, Europe, and Australia making us less exposed to regional problems

Currency Risk

We carry modest currency risk only to the extent that approximately 20-25% of our cash balance may be in US dollars. This risk is modest in the context of our overall balance sheet.

Securitisation Risk

Not relevant. WXL has no positions and is not involved in bundling of securities.

Interest Rate Risk

We have no investments exposing us to interest rate risk other than instant access bank accounts. The interest income earned from these accounts is not a significant proportion of our revenue and has never exceeded 4% of total earnings. Given continued very low interest rates we do not anticipate being exposed to problems arising from a reduction in deposit rates.

Pension Obligation Risk:

WXL does not operate a company final salary pension scheme although all UK based Speedwell group companies satisfy legislation regarding auto enrolment pension contributions. WXL therefore has no exposure as a principal to any defined purchase or money purchase schemes. Contributions to the director’s money purchase scheme have generally been made on an ad-hoc basis. WXL’s balance sheet therefore may from time to time carry cash that is allocated to such investments. This is fully reflected in our accounts.

Given the particularly limited nature of WXL’s risk it is not appropriate to present quantitative results of risk assessment.

Capital Planning

WXL and its parent company plans to maintain a highly liquid position using call bank deposits. It has maintained a policy of organic growth with development funded from internal resources only. No change in this philosophy is anticipated.

Liquidity Planning

WXL and its parent company plans to maintain a highly liquid position using call bank deposits. It has maintained a policy of organic growth with development funded from internal resources only. No change in this approach is anticipated.

COVID-19 Update

The Speedwell group of companies saw little detrimental impact to our business nor to the market we serve that can be directly linked to the economic dislocation arising from the COVID-19 outbreak. The Firm was able to work from home successfully during relevant lock down periods. The economic imperative of removing climate risk seems to continue to drive business and we note that the majority of our clients continue to function as before.

Risk Management Processes

Details of potential risks are set out above.

The main focus is on the quality of data provided through the platform. This is provided to the platform through another Group company and is subject to verification by such company. The Group has been operating in this space for over 20 years and not been litigated against through the quality of the data.

From the point of risk management, the platform will only accept data it believes to be of suitable quality given potential use as part of hedging strategies.

The Group also benefits from all the normal policies such as business continuity, cyber security and financial fraud.

Appendix 1

Stress Testing, Speedwell Group

Impact of market stress on the value of marketable securities:

Zero. We carry no securities.

Ability to meet capital requirements 1 in 25 year event:

- Market conditions: We believe that our ability to trade with no problems (and indeed to expand our client base and increase turnover) during the economic crisis of 2008/9 represents a real-world 1-in-25 year stress test. Our resilience in this downturn is testament to our diverse client base (eg energy as well as banking, as well as insurance) operating across diverse geographies (US, Europe) and to our diverse product base (provision of weather data, weather forecasts, software as well as regulated activities).

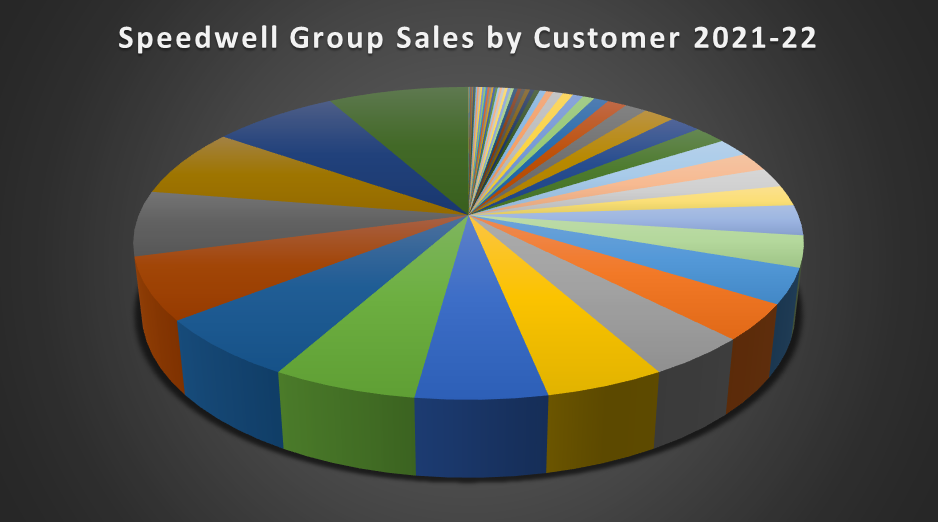

- Impact of loss of biggest client: In 2021-2022 WXL had no direct clients. Revenue is generated from the additional sales of software, pricing data and settlement data to other group companies. Taking the Speedwell group as a whole, we believe that our biggest risk to our capital adequacy relates to the possible loss of a client. The graph below shows that no single client represents more than 10% of total revenue. We have 7 separate clients each with sales of over £200,000 in this year.

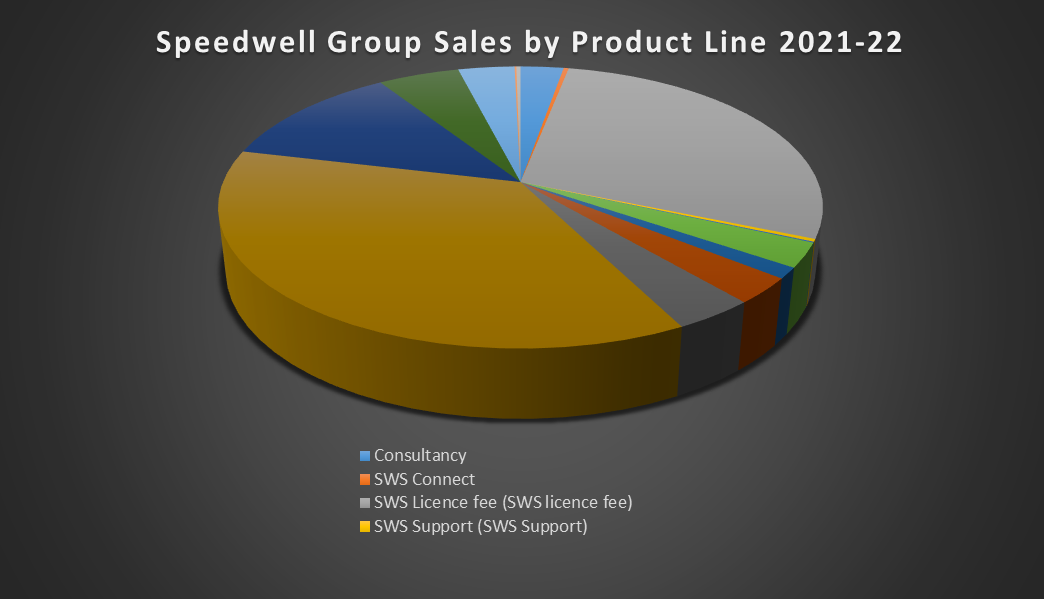

- Impact of Downturn on one of our business areas: The graph below shows the distribution of our revenues across our four key non-regulated activities. We believe this distribution further mitigates against the risk to our business.